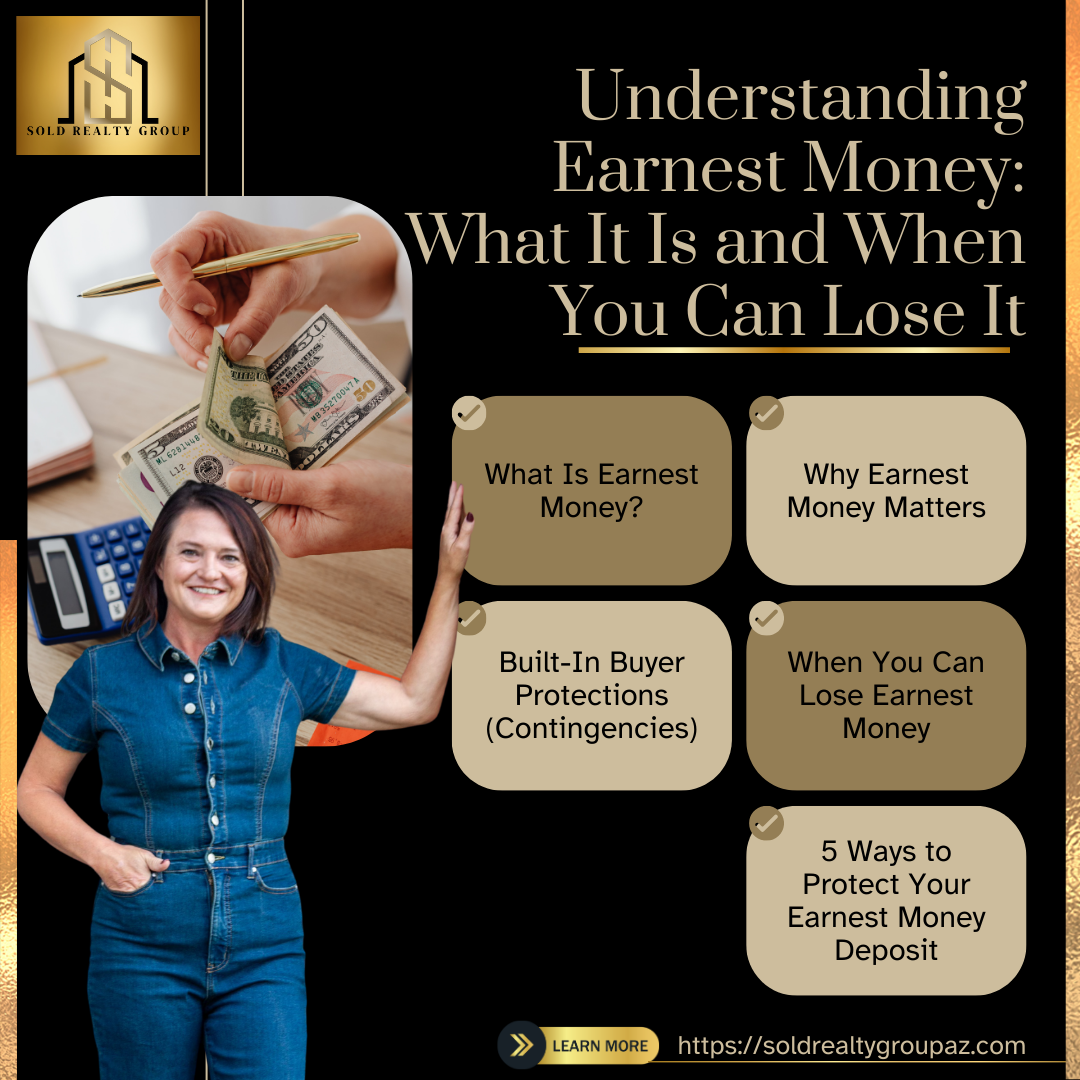

Understanding Earnest Money: What It Is and When You Can Lose It

A must-read for first-time buyers and anyone wanting to protect their wallet — from Sold Realty Group

When you’re ready to make an offer on a home, one of the first things your real estate agent will talk about is earnest money. And if you’re like most buyers—especially first-timers—your first thought might be:

“Wait… do I have to pay that before I even get the house?”

Short answer: Yes. But don’t worry—it’s not money down the drain.

Let’s dive into what earnest money actually is, why it matters, how it works, and most importantly—how to protect it.

💰 What Is Earnest Money?

Earnest money is a “good faith” deposit that accompanies your offer on a home. It tells the seller you’re serious—not just window-shopping—and that you’re financially invested in making the deal work.

This deposit is typically 1% to 3% of the purchase price, but in competitive markets or for luxury homes, it might be more. So, for example:

-

On a $400,000 home, you might offer $4,000 to $12,000 in earnest money.

It’s not an extra fee. If the deal closes, your earnest money gets applied to your closing costs or down payment.

📌 Pro Tip: Earnest money isn’t handed directly to the seller—it’s held in escrow by a neutral third party, like a title company.

🧾 Why Earnest Money Matters

From the seller’s point of view, taking a home off the market is a big deal. They’re turning away other buyers. So your earnest money acts like a “reservation fee” to show you mean business.

✔️ For the buyer:

It helps your offer stand out in a competitive market.

✔️ For the seller:

It’s a sign that the buyer is financially ready and less likely to back out.

⛑️ Built-In Buyer Protections (Contingencies)

Here’s the good news: you don’t lose your earnest money as long as you follow the contract and act in good faith.

There are contingencies written into most offers that allow you to cancel under specific conditions—and still get your money back.

🛠️ Inspection Contingency

You discover major problems during your home inspection (think mold, roof issues, or faulty plumbing). You can back out within the inspection period and keep your earnest money.

💸 Financing Contingency

If you’re pre-approved but your loan is later denied—because of an appraisal gap, job loss, or credit issue—this clause protects you if you notify the seller within the deadline.

🏠 Appraisal Contingency

If the home doesn’t appraise for the full sale price and the seller won’t negotiate, this contingency allows you to walk away and keep your deposit.

📅 Sale of Buyer’s Property (optional)

If your ability to buy depends on selling your current home first, this contingency gives you breathing room.

🚩 When You Can Lose Earnest Money

Earnest money is refundable unless you breach the contract or act outside of the allowed timelines. Here’s how that happens:

❌ Backing out after deadlines pass

If your inspection period ends and then you cancel because of repairs, the seller may keep your deposit.

❌ Buyer’s remorse or “cold feet”

Changed your mind with no valid contingency? That’s on you.

❌ Failure to secure financing without a financing contingency

If you waive the financing clause (common in competitive markets), and your loan falls through, you could lose your earnest money.

❌ Not communicating or missing deadlines

You must notify the seller in writing within the agreed-upon timeframes. Even one missed day can cost you your deposit.

🧠 Real-World Scenario: Who Keeps the Money?

Case 1: Buyer Protected

Inspection shows foundation cracks. Buyer cancels during the 10-day inspection period.

➡️ Buyer gets their earnest money back.

Case 2: Buyer Breaches Contract

Buyer forgets to apply for their loan, misses financing deadline, and can’t close.

➡️ Seller may keep the earnest money as compensation for time lost.

🛡️ 5 Ways to Protect Your Earnest Money Deposit

-

Work with an experienced agent (like yours truly!) who knows how to build in smart protections

-

Stick to deadlines—set calendar reminders for contingency periods

-

Get everything in writing—verbal notices don’t count

-

Don’t waive contingencies unless you’re financially secure enough to cover surprises

-

Ask before you assume—when in doubt, let your agent guide your next step

🤝 The Bottom Line

Earnest money is a normal part of homebuying, and when used correctly, it’s a tool to strengthen your offer—not a risk to fear. With the right protections in place, it’s fully refundable under the right circumstances.

At Sold Realty Group, we make sure every client understands what they’re signing, what their timeline is, and how to protect their investment at every step.

You should never feel confused—or worse, blindsided—by something like earnest money. And with us in your corner, you won’t.

Ready to Shop Smart and Buy Confidently?

Let’s talk about your goals and get your dream home under contract—with your money protected and your mind at ease.

📍 Mesa & East Valley | Serving Phoenix, Queen Creek, San Tan Valley

📞 April at (480) 309-4322

🌐 soldrealtygroupaz.com

📧 [email protected]

Categories

- All Blogs (239)

- Arizona Real Estate & Local Market (19)

- Buying, Selling & Investing Tips (77)

- Home Improvement Ideas (40)

- HOME MAINTENACE TIPS (22)

- Home Selling Strategies (26)

- Legal & Financial Consideration (11)

- Listing (5)

- Living in Queen Creek (15)

- LIVING IN SANTAN VALLEY (12)

- Local Business Spotlight (2)

- Local Events & Activities (3)

- Question & Answers (1)

- Real Estate Education & Empowerment (8)

- SANTAN VALLEY (1)

- Sold Selling Method: Perception (5)

- Sold Selling Method: Presentation (5)

- Sold Selling Method: Price (3)

- Staging (14)

- Sustainability and Green Living (4)

Recent Posts

GET MORE INFORMATION